This is the translation of this post published in January, 2019. It is a rather long article and I apologize for this, thanking those who will reach its end.

As any buzzword worthy of its name, also Digital Transformation or DX gave birth to a galaxy of definitions from the IT-oriented ones by tech giants such as IBM focusing on Big Data, AI, IoT, blockchain to the market-oriented ones by big management consulting firms focusing on market aspects such as disruption or the blurring of boundaries between enterprise, its suppliers and its clients.

However I (*) fell in love with a very visual one, whose author, sadly, I don’t know:

Digitization paved cowpaths, making enterprise processes more efficient, but DX turns caterpillars into butterflies.

Anonymous

So we saw torrents of digitization but only trickles of DX in the Financial Sector (always ready to turn atoms in bits) in Healthcare and Marketing (driven by the growing ability to collect ever larger masses of data on larger populations of increasingly connected individuals, and in Manufacturing /thanks to the progressive replacement of analog machinery and measurement tools with their digital and connected brethren).

But never and nowhere we have yet seen a caterpillar turn into a butterfly, as it’s happening now under our vey noses in the Automotive Sector where the building blocks of ADX are parading in front of us: the replacement of the majority of mechanical (and therefore, inherently analog) components with electrical and electronic (and therefore, inherently digital) components; the disruption of the manufacturing process itself, from powertrain-centric to battery-centric (if nothing else, for reasons of weight); the pervasiveness of sensors; the ubiquity of connections; the growing use of Artifical Intelligence.

The skin of the caterpillar (i.e. what we shed)

Obviously the industry won’t come out unscathed from this earthquake: what are we to do with the parts suppliers who make transmission shaft or belts, lubricants and filters for gasoline, oil or water? The SKU list of an Internal Combustion Engine (ICE) car can include over 30.000 items, while an electric (EV) car rarely surpasses 10.000 !

What will be the destiny of those who manufacture mufflers, radiators, clutches and tanks? One such company recently told us that the long term orders (who are vital to make sure the immense quantities of these parts reach carmakers plants right when they are needed) stop at 2020 as if afterwards…. hic sunt leones!

When we think that the Automotive industry (especially the all-relevant German bit) sources from world leading Italian parts manufacturers, maybe we, as a Country, should worry a little bit about this.

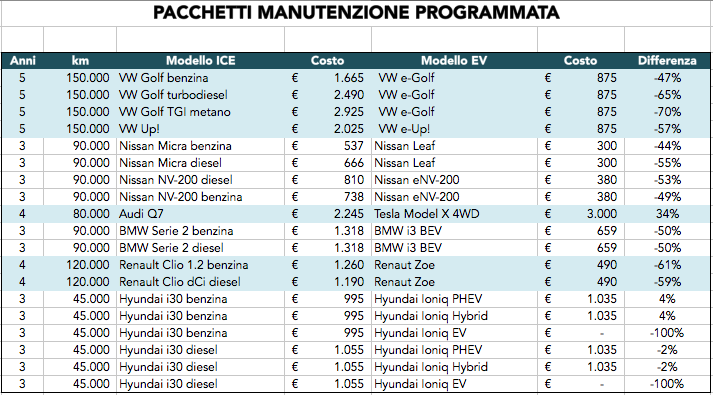

Nor the after sales services sector will fare much better: in this table we collected programmed maintenance costs as quoted by the carmakers themselves, comparing each EV model with its ICE equivalent, showing decreases ranging from 50% to 100%.

A major insurance broker explained during the ANCI-sponsored training courses on Electric Mobility that the different driving style justifies a significant discount due to lower riskiness of insurance policies for electric cars.

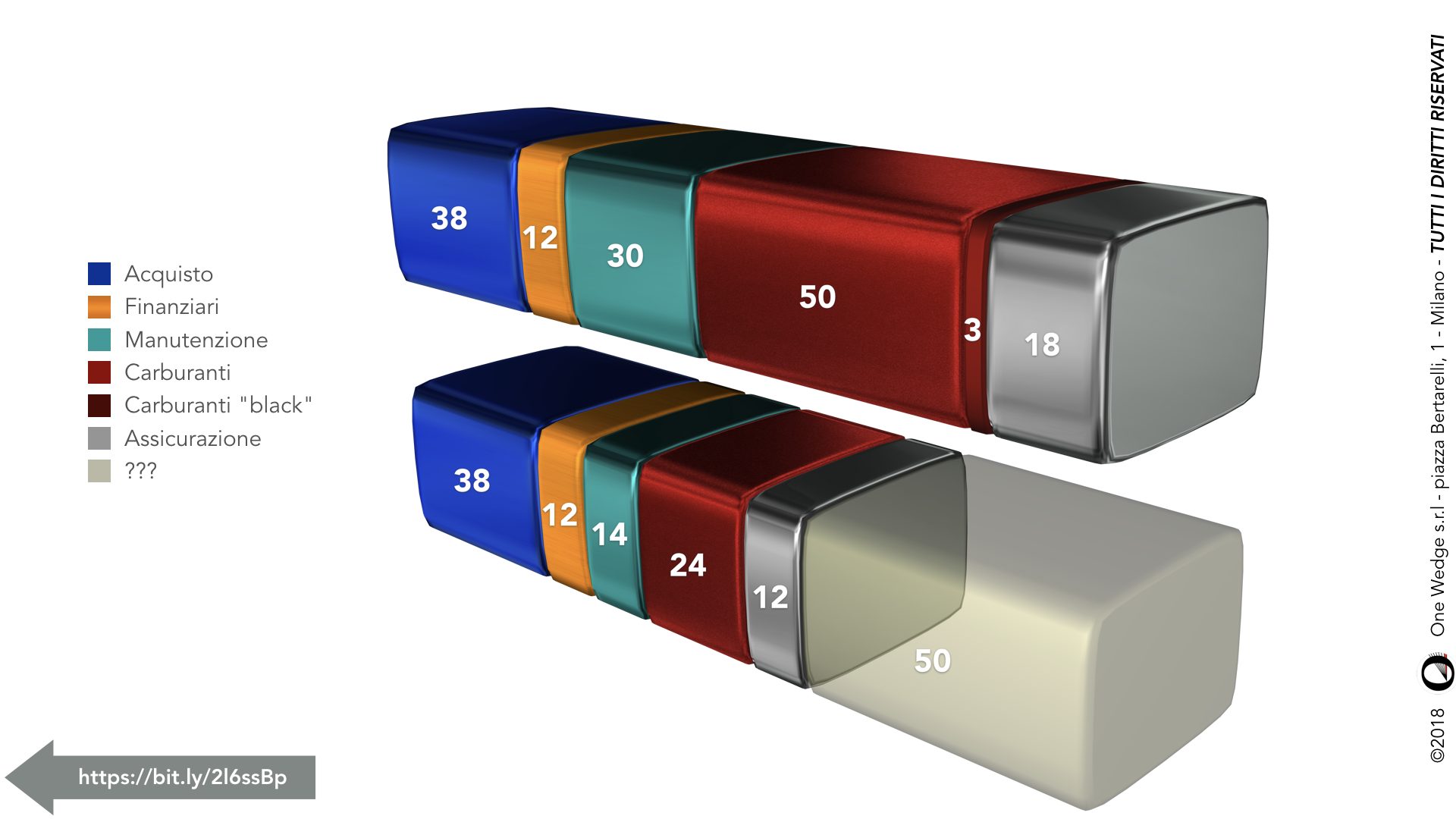

To sum it up, the full value chain will move or lose altogether between 50 and 100 billion euros PER YEAR, in Italy alone; considering the Boot represent about 2.5% of the global auto industry, it’s easy to estimate the impact on a planetary scale.

The wings of the butterfly (i.e. what we gain)

So what’s on the other side?

First of all, immense environmental benefits: you will forgive if those who (like yours truly) live in the most polluted area in Europe think that this is Number One!

It’s a topic I covered so often I can’t do it again (I’d rather link some of those earlier articles like this (italian only, sorry) which could be condensed ina slogan:

Do away with 75%

of the second-largest pollution source

in urban environments

A different driving style

It’s enough to drive an electric car for a few days (and everybody can try, thanks to the many sharing services available in all major cities) to realize how the driving style morphs. It’s a bit like moving from a stick-shift to an auto gearbox: there is some diffidence at the onset but once you try you don’t go back!

Refueling an ICE car it’s always done in the same way: you stop, you fill the tank, you leave after very few minutes. Refueling an EV instead is first of all an occasional event: the average car registered in Italy drives about 11.000 km per year which, divided by 200 usage days yields about 50 kilometers per day, well within the range of even the smallest EVs.

Those who live in a house or have a garage therefore will mostly recharge their EVs during the night and rarely stop at a service station; by the wy, this would shift the electrical load due to cars to nighttime, when the grid is vastly under-utilized and electrical energy cheaper.

And when you do stop, the experience of highways demonstrates that in a so-called complex stop ancillary services become important and offer opportunities to further monetize a 30-minutes visit: food, drinks, personal services, entertainment become mandatory corollaries and – perhaps – the reason why you choose one station over another, much in the same way fidelity programs play a role to retain department store or supermarket patrons.

Moreover, charge services could become remunerated through a flat contract, similarly to what happened to other services once associated with a counter such as telephony or home video.

An EV also enables the so-called one-pedal-driving: the ability to recuperate when braking a good portion of the kinetic energy accumulated on the vehicle develops a quite different driving style especially in urban areas. The vehicle is slowed down without the use of the brake (lowering the consumption of brake pads) and the driver is more alert because s/he is trying to anticipate the traffic conditions which may require slowing.

What about when we won’t drive at all?

In my view, this is inevitable although not close in time: I have no doubt that a computer has the potential for being a better driver than a human given the fact it does not tire, can’t drink too much or sleep too little and – most importantly – always obeys all the rules.

Having said all this, however, experience (**) suggests that the path to Artifical Intelligence is quantum asymptotic: asymptoticbecause it gets closer and closer to the target without ever fully reaching it and quantum because during this long march it achieves intermediate targets of significant practical value.

Such intermediate results may include initially repetitive tasks such as “park the car in my garage” or “drive on the highway all the way to Bologna” to be subsequently followed by autonomous driving of increasing complexity and domain unbound, i.e. increasingly exposed to unforeseeable events such as city traffic or mountain driving.

Such increasingly autonomous vehicles will pick us up at our doorstep, will drop us at our destination and will go seek a parking spot perhaps picking the one where refueling is cheapest, should it need juice. Their maintenance on the few remaining part where wear will continue to happen (obviously all software will update over-the-air as for our computers or telephones) will be managed by sophisticated predictive algorithms supported by the fact that at every recharge the whole log may be read and analysed to diagnose potential upcoming failures, enabling programming visits to maintenance centers, perhaps even during the night when the car is not in use.

An industrial policy challenge

The caterpillar is becoming a butterfly and nobody can stop this, but we can thank our luck that the transformation will last many decades, giving us the opportunity to prepare for the butterfly world while we still live in the caterpillar world.

To be honest, nobody really knows how long it will take: we can estimate a lower limit of about 18 years (there are 36 million cars on Italian roads, and 2 millions are sold each year), but innovations usually follow a variable velocity accretion curve called a sigmoid (or S-curve). The sigmoid suggested by historical data (not abundant enough to offer any confidence) seems to indicate we could stop selling ICE cars sometimes around 2030.

Let’s hope this prediction is correct as the task ahead of us is titanic: converting auto manufacturing means converting plants and machinery, but it also means re-skilling workers which may require a radical redesign of our intermediate and upper education system.

We should not take decades for granted: on july, 15th 1886 Karl Benz filed a patent in Mannheim for the first ICE car, but after only 22 years in New York (half a world away) the number of motor cars had already equalled the number of horse-drawn carriages.

NOTES

(*): To explain why I consider myself fit to discuss this matter, I need to bring up my bio. I come from Marketing and Communications, and Information Technology before that: these two areas of expertise merged during the years I dealt with Digital Transformation, crystallizing it all in two small manuals on digital identity and on the governance of digital transformation processes. I realize today that Electric Mobility in this respect is in seamless continuity with my previous experiences.

(**) specifically, a multi-year collaboration with one of the hottest german AI start-ups

Una risposta a "The Automotive Digital Transformation"